This is an excellent research topic because an Initial Public Offering (IPO) is one of the most complex milestones in a company’s life. A successful IPO requires years of preparation involving corporate governance, finance, law, technology, cybersecurity, investor relations, compliance, auditing, and strategic planning.

Below is a comprehensive IPO framework comparing four of the world’s major capital markets:

- Johannesburg Stock Exchange (JSE)

- United States (New York Stock Exchange and Nasdaq)

- Asia (major exchanges including Tokyo Stock Exchange, Hong Kong Stock Exchange, Singapore Exchange, Shanghai Stock Exchange, and National Stock Exchange of India)

- London Stock Exchange

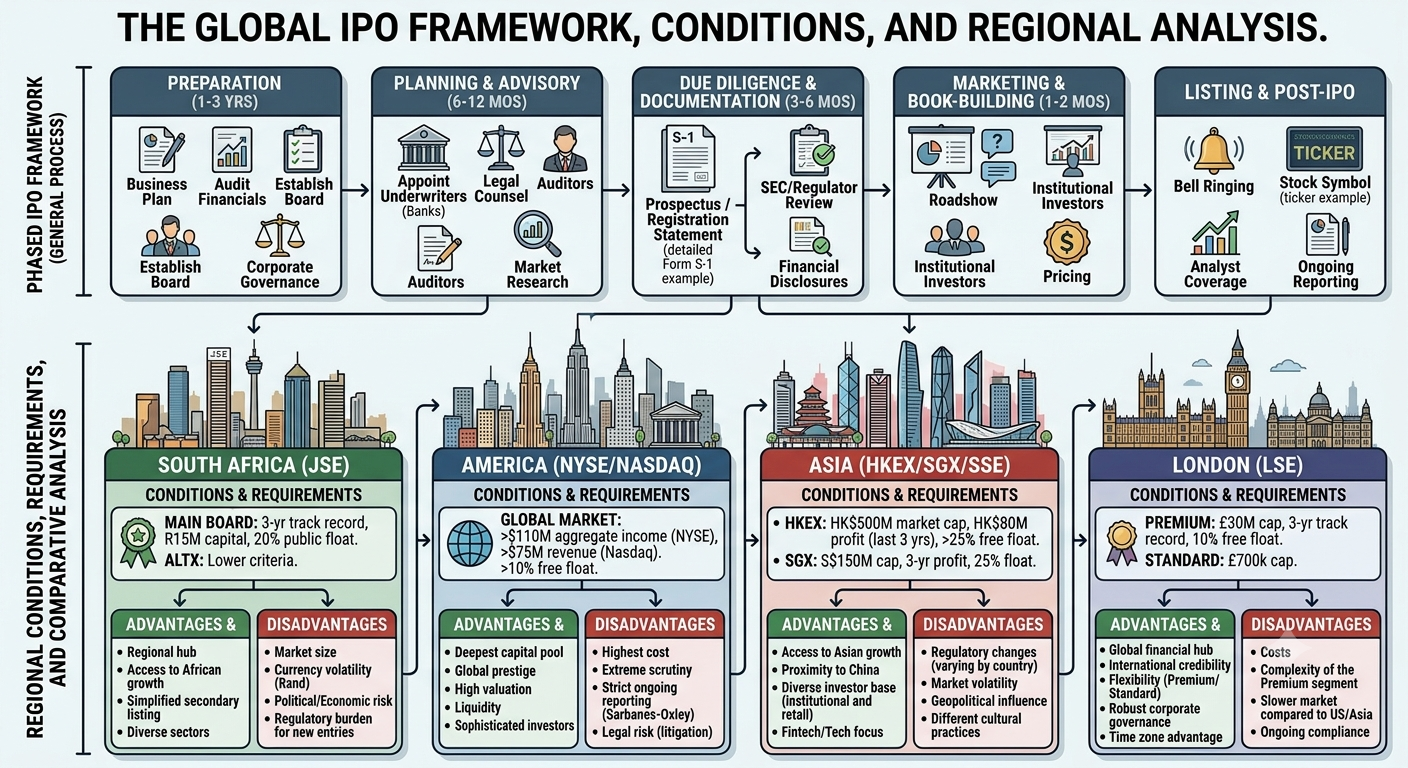

MASTER IPO FRAMEWORK

A complete IPO generally consists of 12 major phases and more than 250 individual tasks.

Phase 1 — Business Maturity

The company should have:

- Sustainable revenue

- Consistent growth

- Profitable operations (or a credible path to profitability where permitted)

- Competitive advantage

- Strong market share

- Scalable business model

- Experienced management

- Ethical corporate culture

- Clear long-term strategy

- Risk management framework

Phase 2 — Corporate Governance

Before listing, companies usually establish:

- Independent board

- Executive directors

- Non-executive directors

- Audit committee

- Risk committee

- Nomination committee

- Remuneration committee

- ESG committee

- Internal audit

- Compliance office

- Ethics office

Phase 3 — Financial Requirements

Typical expectations include:

- Audited financial statements (generally 3 years where applicable)

- Clean audit opinions

- International accounting standards (such as IFRS in many jurisdictions)

- Strong cash flow management

- Working capital assessment

- Internal financial controls

- Budget forecasts

- Capital allocation plan

- Tax compliance

Phase 4 — Legal Preparation

The company must review:

- Intellectual property

- Litigation risks

- Employment contracts

- Shareholder agreements

- Licensing

- Environmental compliance

- Competition law

- Data privacy compliance

- Regulatory approvals

Phase 5 — IPO Team

Typical advisers include:

- Investment banks

- Legal advisers

- Auditors

- Tax advisers

- Investor relations advisers

- Public relations specialists

- Transfer secretaries

- Listing sponsor (required in some markets)

- Underwriters

- Valuation specialists

Phase 6 — Prospectus

The prospectus normally contains:

- Business description

- Industry analysis

- Risk factors

- Financial statements

- Governance

- Executive compensation

- Shareholding structure

- Use of proceeds

- Dividend policy

- Legal disclosures

Phase 7 — Regulatory Review

Regulators evaluate:

- Disclosure quality

- Financial accuracy

- Accounting standards

- Governance

- Risk disclosure

- Market transparency

- Investor protection

Phase 8 — Marketing

Often called the roadshow:

- Institutional investor meetings

- Retail marketing

- Media engagement

- Analyst presentations

- Pricing discussions

- Book-building

Phase 9 — Pricing

Investment banks determine:

- IPO valuation

- Share price

- Shares offered

- Market capitalization

- Demand assessment

Phase 10 — Listing Day

Activities include:

- Shares begin trading

- Opening price established

- Market stabilization (where applicable)

- Investor communications

- Ongoing disclosures begin

Phase 11 — Post-IPO

The company must maintain:

- Quarterly or semiannual reporting (depending on market)

- Annual reports

- Governance reviews

- Continuous disclosures

- Shareholder meetings

- ESG reporting where required

Phase 12 — Long-Term Public Company Management

Public companies continuously manage:

- Shareholder relations

- Acquisitions

- Capital raising

- Dividends

- Secondary offerings

- Credit ratings

- Strategic growth

SOUTH AFRICA (JSE)

Typical Requirements

- Public company status

- Adequate shareholder spread

- Sufficient public float

- Audited financial history

- Corporate governance aligned with the Institute of Directors in South Africa’s King Code

- IFRS financial reporting

- Listing sponsor

- Independent directors

- Ongoing disclosure obligations

Advantages

- Gateway into African capital markets

- Strong institutional investor base

- Well-developed regulatory environment

- International credibility

- Improved access to capital

- Increased company profile

Disadvantages

- Smaller liquidity than the largest global exchanges

- Significant compliance costs

- Ongoing governance obligations

- Greater public scrutiny

UNITED STATES (NYSE/Nasdaq)

Typical Requirements

- Higher governance expectations

- Extensive regulatory disclosure

- Audited financial statements

- Internal controls

- Independent directors

- Audit committee

- Market capitalization and shareholder distribution requirements (vary by exchange and listing standard)

Advantages

- World’s deepest capital markets

- Highest liquidity

- Global visibility

- Large institutional investor participation

- Higher valuation potential for many companies

- Access to significant growth capital

Disadvantages

- Very expensive IPO process

- Intensive regulatory oversight

- Higher litigation risk

- Extensive reporting obligations

- Significant compliance costs

ASIA

Requirements vary across exchanges but commonly include:

- Audited financial history

- Governance standards

- Profitability or alternative listing criteria (depending on exchange)

- Public float requirements

- Independent directors

- Continuous disclosure

Advantages

- Access to fast-growing economies

- Large investor populations

- Strong technology investment ecosystems

- Regional expansion opportunities

Disadvantages

- Different regulatory regimes

- Geopolitical considerations

- Currency risks

- Varying disclosure requirements

LONDON STOCK EXCHANGE

Typical expectations include:

- Corporate governance under UK standards

- Audited financial statements

- Independent board oversight

- Public float requirements

- Comprehensive prospectus

- Ongoing disclosure

Advantages

- Global financial centre

- Strong institutional investor participation

- International credibility

- Access to European and global capital

Disadvantages

- High compliance costs

- Intense governance expectations

- Market volatility

- Competitive listing environment

Comparative Summary

| Feature | South Africa (JSE) | United States | Asia | London |

|---|---|---|---|---|

| Cost of IPO | Medium | Very High | Medium to High | High |

| Liquidity | Medium | Very High | High | High |

| Investor Base | African & Global | Global | Regional & Global | Global |

| Regulatory Burden | High | Very High | Medium to High | High |

| Prestige | High in Africa | Very High | High | Very High |

| Capital Raising Potential | High | Very High | High | Very High |

| Ongoing Reporting | High | Very High | High | High |

Common Reasons IPO Applications Are Delayed or Rejected

- Inadequate financial controls

- Weak corporate governance

- Incomplete disclosures

- Unresolved legal disputes

- Material accounting issues

- Poor internal controls

- Insufficient public float

- Regulatory non-compliance

- Cybersecurity weaknesses

- Inexperienced management

- Unsustainable business model

Advantages of Going Public

- Access to large pools of capital

- Increased public profile and brand recognition

- Liquidity for founders and early investors

- Easier future fundraising

- Acquisition currency through listed shares

- Employee share incentive programmes

- Greater transparency and credibility

- Improved access to debt financing

- International expansion opportunities

Disadvantages of Going Public

- Loss of some managerial flexibility due to shareholder oversight

- Expensive IPO process

- Ongoing reporting and compliance costs

- Pressure to meet market expectations

- Risk of hostile takeovers

- Greater regulatory scrutiny

- Potential shareholder activism

- Public disclosure of sensitive business information

- Increased cybersecurity and governance obligations

- Management time devoted to investor relations

For a doctoral-level (100+ page) thesis, this framework can be expanded into approximately 25 chapters, covering IPO strategy, corporate governance, financial reporting, valuation methods, underwriting, legal compliance, environmental, social and governance (ESG) reporting, technology and cybersecurity, investor relations, post-listing obligations, and detailed comparisons of listing rules across South Africa, the United States, Asia, and the United Kingdom.

Be First to Comment