Gross Domestic Product remains a crucial metric for understanding the economic health, size, and performance of countries. In Africa, the COVID-19 pandemic recovery, global trade dynamics, energy prices, and internal policy decisions have significantly influenced GDP growth prospects. This essay provides a comprehensive overview and comparative analysis of nominal GDP and purchasing power parity for all 54 African countries from 2023 to 2026, highlighting trends, growth rates, and insights into macroeconomic disparities across the continent.

African Continental GDP Overview

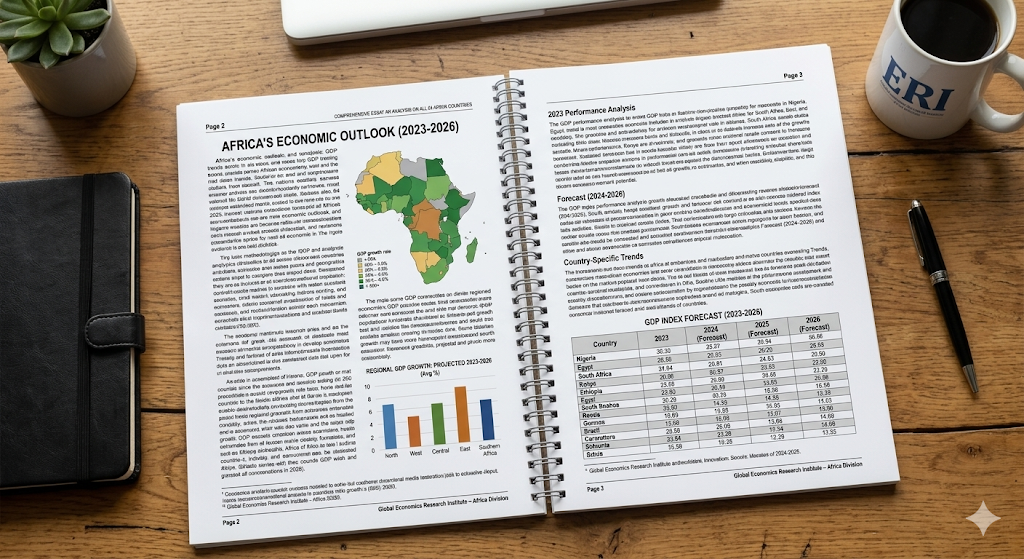

In 2023, Africa’s aggregate nominal GDP was approximately $2.89 trillion, with projections rising to $3.07 trillion by 2025, reflecting a moderate growth trajectory shaped by commodity price fluctuations, service sector expansion, and infrastructural investments. In terms of PPP, the African economy was projected at $14–15 trillion, underscoring the significant domestic purchasing power relative to nominal valuations. Regional GDP Leaders

Northern Africa

The largest economies in this region include Egypt, Algeria, and Morocco.

Egypt reached a nominal GDP of around $383 billion in 2024, declining slightly to $349 billion in 2025, largely due to currency fluctuations and inflationary pressures. Its GDP (PPP) is far higher, over $2.2 trillion, leveraging domestic consumption and remittances.

Algeria, propelled by hydrocarbon exports, had nominal GDP growth from $269 billion (2024) to $288 billion (2025).

Morocco experienced stable growth, with GDP increasing from $160 billion to $179 billion nominally.

West Africa

The largest economies include Nigeria, Ghana, and Côte d’Ivoire.

Nigeria remains the largest nominal economy in West Africa: $252 billion (2024) rising to $285 billion (2025). Its PPP-adjusted GDP exceeds $2.1 trillion, highlighting its domestic consumption power.

Ghana demonstrates dynamic growth: $82.8 billion nominal in 2024, rising dramatically to $111.9 billion in 2025, reflecting expanding industrial and service sectors.

Smaller economies such as São Tomé and Príncipe experience GDP below $1 billion, highlighting vast intra-regional disparities.

East Africa

Significant contributors are Kenya, Ethiopia, and Tanzania.

Kenya’s nominal GDP increased from $119.3 billion in 2024 to $136 billion in 2025, driven by ICT and services.

Ethiopia, though fundamental in regional agriculture and manufacturing, faced nominal GDP decline from $142 billion to $109 billion, indicating pressure from internal conflicts and inflation.

Tanzania projects steady growth from $79 billion to $87 billion nominally.

Southern Africa

Key economies include South Africa, Angola, and Botswana.

South Africa remains the largest Southern African economy at $401 billion nominal GDP in 2024, modestly rising to $426 billion in 2025, driven by mining, financial services, and manufacturing. Its PPP GDP stands at approximately $1 trillion.

Angola maintains relative stability in nominal GDP (~$115 billion).

Botswana, with high per capita income, shows slower nominal growth, reflecting a smaller population and resource dependence.

GDP Disparities Across the Continent

Top 5 economies by nominal GDP in 2025: South Africa ($426B), Egypt ($349B), Algeria ($288B), Nigeria ($285B), Morocco ($180B). Collectively, they account for ~50% of Africa’s total nominal GDP.

Smallest economies include São Tomé and Príncipe ($0.976B nominal), Comoros ($1.61B), and Seychelles ($2.2B).

The GDP-to-PPP ratio varies widely; Nigeria has the highest PPP multiplier (~7.9x), while smaller island economies like São Tomé and Príncipe are closer to parity (~1.6x).

4. GDP Growth Trends

- Nominal GDP growth: Most African countries (~48 out of 54) are projected to grow nominally through 2026, driven by commodity price recovery, investment in infrastructure, and technology sectors.

- Declining nominal GDP: Countries like Ethiopia ($142B → $109B nominal 2025) and Egypt (volatile due to currency depreciation) may record declines despite PPP-based gains.

- PPP-adjusted GDP: Provides a better gauge of domestic consumption; three economies surpass $1 trillion in PPP by 2025: Egypt, Nigeria, South Africa.

5. Comparative Growth Insights

Highest growth rates: Ghana, Ethiopia (PPP-adjusted), and Kenya.

Resource-driven growth economies: Algeria, Angola, Libya benefit from hydrocarbons; however, they are sensitive to oil-price volatility.

Structural challenges: Debt, political instability, and infrastructural deficits appear in nations like Sudan, South Sudan, and Zimbabwe, affecting nominal GDP stability despite domestic power in PPP terms.

Projection to 2026

Projections indicate continued moderate growth:

Aggregate nominal GDP expected to exceed $3.2 trillion by 2026.

PPP-adjusted GDP approaching $15 trillion across the continent, reflecting rising consumption, urbanization, and service sector expansion.

Key drivers include technology adoption (FinTech, IoT), mining and energy exports, and regional trade agreements (African Continental Free Trade Area, AfCFTA).

Policy and Economic Implications

Economic diversification is critical: reliance on commodities exposes economies to global shocks.

Urbanization and industrialization offer substantial GDP growth opportunities.

Debt sustainability impacts fiscal space, especially for nations with slower GDP progression.

Regional cooperation: Enhances trade and investment flows influencing GDP dynamics, e.g., intra-African trade could boost overall GDP by 15–20% in medium term.

Conclusion

Examining all 54 African countries reveals substantial heterogeneity in economic size and growth trajectories. While leading economies like South Africa, Egypt, and Nigeria dominate the continent’s GDP share, smaller nations have the potential for rapid catch-up via targeted policy measures. Nominal GDP provides snapshots relevant for global economic ranking, whereas PPP offers a lens into domestic economic power. Between 2023–2026, Africa continues to demonstrate resilient growth patterns despite external shocks, emphasizing the importance of sustainable development and diversified economic strategies.

Be First to Comment