Introduction: The Hidden Elements of the Digital Age

In the intricate web of modern technology, three relatively obscure elements have emerged as indispensable components of our digital civilization: gallium, germanium, and antimony. While silicon commands the spotlight in discussions about semiconductors, these three minerals quietly enable the advanced capabilities that define contemporary electronics, telecommunications, defense systems, and renewable energy infrastructure. Their importance has transcended purely technical considerations to become matters of national security and economic strategy, particularly as geopolitical tensions have exposed the fragility of global supply chains.

These elements share remarkable characteristics that make them critical to modern industry: they are relatively rare, difficult to extract as primary products, and possess unique physical and chemical properties that cannot be easily replicated by substitutes. Understanding their origins, properties, and applications reveals not only the sophistication of modern technology but also the complex interdependencies that characterize our globalized economy.

Part One: Gallium – The Liquid Metal of the Future

Discovery and Historical Development

Gallium’s discovery in 1875 by French chemist Paul-Émile Lecoq de Boisbaudran represents one of the most remarkable validations of Dmitri Mendeleev’s periodic table. Working in his laboratory in Paris, Lecoq de Boisbaudran observed two distinctive violet spectral lines while examining zinc blende ore from the Pyrenees Mountains. This discovery occurred just four years after Mendeleev predicted the existence of an element he called “eka-aluminium” based on gaps in his periodic table.

What made this discovery particularly significant was how precisely the actual properties of gallium matched Mendeleev’s predictions. Initially, de Boisbaudran measured gallium’s density as 4.7 g/cm³, but after Mendeleev wrote suggesting he remeasure it, de Boisbaudran obtained 5.9 g/cm³, exactly as Mendeleev had predicted. This dramatic confirmation strengthened confidence in the periodic table as a predictive tool and marked the beginning of modern systematic chemistry.

The element’s name carries a touch of patriotic pride and possible wordplay. Lecoq de Boisbaudran named it gallium after Gallia, the Latin name for France. Some historians have noted that “Lecoq” translates to “the rooster” in French, and the Latin word for rooster is “gallus,” suggesting the name may have been a subtle self-reference as well.

Physical and Chemical Properties

Gallium possesses several extraordinary physical properties that have fascinated scientists for nearly 150 years. Its melting point of 29.7646 °C means it liquefies just above room temperature and can melt in one’s hand. This remarkably low melting point, combined with an extraordinarily high boiling point around 2,400°C, gives gallium one of the widest liquid ranges of any element, spanning approximately 2,000 degrees Celsius.

Like water, gallium exhibits the unusual property of expanding as it freezes, which requires careful consideration when storing liquid gallium in sealed containers. In its solid state at room temperature, gallium is a soft, silvery-blue metal that fractures in shell-like patterns, a characteristic known as conchoidal fracturing.

Early Applications and the Semiconductor Revolution

From its discovery in 1875 until the semiconductor era, gallium’s primary uses were in high-temperature thermometers and metal alloys with unusual melting properties. Its non-toxic nature made it an ideal replacement for mercury in certain applications, and various gallium alloys remain liquid at or below room temperature.

The transformative moment for gallium came in the 1960s with the development of gallium arsenide as a direct bandgap semiconductor. The 1952 synthesis of gallium arsenide crystals at Siemens revealed electron mobility six times greater than silicon, fundamentally reshaping electronics. This superior performance at high frequencies meant that where silicon transistors struggled at 100 MHz, early gallium arsenide devices achieved 1 GHz operation by 1954.

This breakthrough opened entirely new technological frontiers. Gallium arsenide’s superior high-frequency performance made it indispensable for satellite communications, military radar systems, and eventually the mobile phone revolution. The material proved particularly valuable for applications requiring both speed and efficiency under demanding conditions.

Modern Applications: The Backbone of Advanced Technology

Today, gallium stands as one of the most critical materials in modern electronics. Its applications span multiple high-technology sectors:

Semiconductors and High-Speed Electronics: Gallium arsenide and gallium nitride semiconductors power a vast array of devices. These compounds enable the high-frequency operations essential for 5G telecommunications infrastructure, satellite communications, and advanced radar systems. The superior electron mobility of gallium-based semiconductors allows them to operate at frequencies and temperatures where silicon-based alternatives would fail.

Optoelectronics and Lighting: By 1962, Nick Holonyak Jr.’s demonstration of the first visible LED marked gallium’s entry into the photonics age. Today, gallium nitride and indium gallium nitride compounds produce the blue and violet light-emitting diodes that, when combined with phosphors, create the white LED lighting that has revolutionized illumination technology. These same compounds enable blue laser diodes used in Blu-ray players and high-density data storage.

Solar Energy: Gallium arsenide solar cells on the Apollo 11 lunar module proved the element’s resilience in the harshest environments imaginable. Modern space missions rely heavily on gallium-based photovoltaics because they offer higher efficiency than silicon alternatives and maintain performance under intense radiation. Triple-junction solar cells incorporating gallium achieve conversion efficiencies exceeding 30%, making them ideal for space applications and concentrated solar power systems.

Defense and Aerospace: Military applications represent some of the most demanding uses of gallium-based technologies. Advanced radar systems, electronic warfare equipment, missile guidance systems, and secure communications all depend on gallium compounds for their high-frequency, high-power performance.

Global Supply and Geopolitical Significance

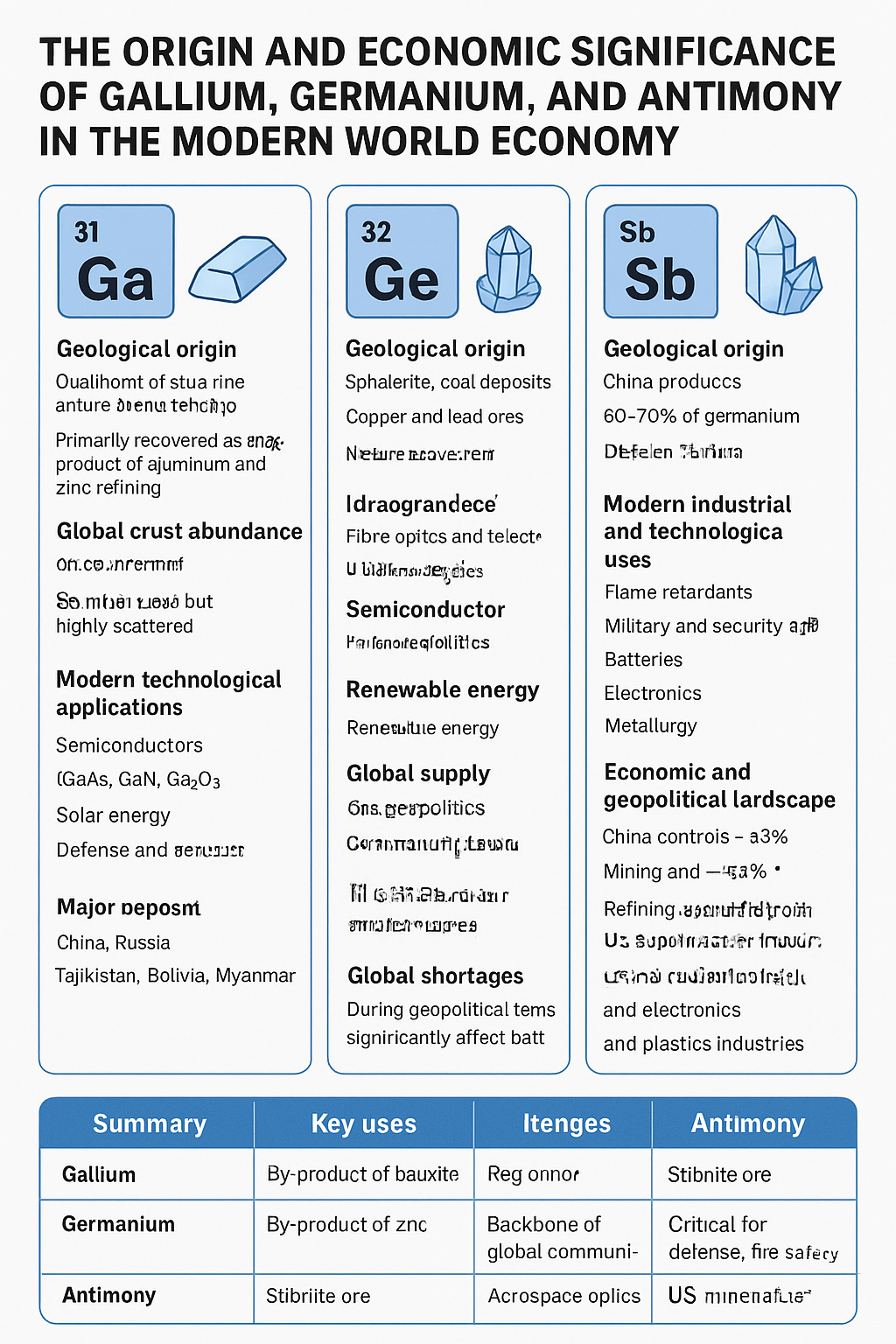

China controls approximately 98% of global gallium production and 90% of refining capacity, creating an extraordinary concentration of supply. This dominance stems not from overwhelming reserves but from China’s control of aluminum and zinc production, as gallium is primarily recovered as a byproduct of processing these metals.

Gallium doesn’t occur free in nature and is extracted as a byproduct from zinc blende, iron pyrites, bauxite, and germanite. The element exists in trace amounts in these ores, making dedicated gallium mining economically unviable. Recovery rates are typically low, with very low amounts (less than 3%) of gallium contained in zinc ores being recovered worldwide.

The concentration of gallium production in China has become a significant concern for Western nations. The United States imports almost 95% of its gallium from China, creating vulnerability to supply disruptions. When Beijing imposed export restrictions in 2023 and later banned exports to the United States in December 2024, it demonstrated how critical minerals could be weaponized in geopolitical competition.

The US Geological Survey calculated that if China were to halt all gallium exports, the US GDP could face a decline of $3.4 billion. This economic impact extends beyond direct manufacturing losses to encompass disruptions throughout technology supply chains, from consumer electronics to military equipment.

Part Two: Germanium – Silicon’s Sophisticated Cousin

Discovery: Validating the Periodic Table

In 1869, Dmitri Mendeleev predicted the existence of an element he called ekasilicon, forecasting it would have an atomic weight around 72 and specific properties based on its position between silicon and tin. This prediction would wait 17 years for confirmation.

In mid-1885, a new mineral was discovered at a mine near Freiberg, Saxony. A miner passed the unusual ore to mineralogist Albin Weisbach, who confirmed it as a new mineral, later known as argyrodite. His colleague Clemens Winkler analyzed it and found it consisted of 75% silver, 18% sulfur, and a mysterious 7% that couldn’t be explained.

By February 1886, Winkler realized he had discovered a new element and named it germanium, honoring his homeland. Initially, Winkler considered naming it neptunium after the recently discovered planet Neptune, but that name had already been proposed for another element.

Winkler prepared several compounds including fluorides, chlorides, sulfides, dioxide, and tetraethylgermane, the first organogermane. The physical data from these compounds corresponded remarkably well with Mendeleev’s predictions, providing crucial validation of the periodic law and demonstrating the power of systematic chemistry.

From Scientific Curiosity to Strategic Material

Until the late 1930s, germanium was thought to be a poorly conducting metal and did not become economically significant until after 1945, when its properties as an electronic semiconductor were recognized. During World War II, small quantities were used in specialized electronic devices, primarily diodes for radar pulse detection.

Research on germanium’s electrical properties during the 1920s paved the way for the development of high-purity, single-crystal germanium eventually used as rectifying diodes in microwave radar receivers. This wartime research proved critical for the Allied victory, enabling more effective radar systems that provided crucial advantages in detecting enemy aircraft and ships.

The post-war period brought germanium’s most significant breakthrough. Germanium’s first commercial application came immediately after the war when John Bardeen, Walter Brattain, and William Shockley invented the first transistor at Bell Labs in 1947. This invention, which earned them the Nobel Prize in Physics, launched the modern electronics age and positioned germanium as the semiconductor material of choice for the electronics industry.

For the next two decades, germanium dominated semiconductor manufacturing. Transistor radios, hearing aids, early computers, and telecommunications equipment all relied on germanium-based components. The material’s properties made it ideal for these early applications, though it would eventually be largely superseded by silicon for most mainstream applications.

Unique Properties and Characteristics

Germanium is a lustrous, hard, grayish-white metalloid that occupies a middle ground between metals and non-metals. It is intermediate in properties between metals and nonmetals, sharing chemical similarities with silicon. Like gallium, germanium has the unusual property of expanding as it freezes, along with only four other elements: silicon, bismuth, antimony, and gallium.

Germanium exists as neutral species in acidic pH environments, requiring special extraction techniques using organic ligands to form anionic germanium-ligand complexes. This unusual behavior complicates recovery processes and contributes to the element’s relatively high cost.

The element ranks approximately 50th in abundance in Earth’s crust and seldom appears in high concentrations. Primary minerals include argyrodite, germanite, renierite, and canfieldite, all of them rare. Like gallium, germanium is primarily recovered as a byproduct, in this case from zinc refining and coal combustion residues.

Contemporary Applications

While silicon has displaced germanium in many conventional semiconductor applications, germanium maintains critical niche roles where its unique properties provide distinct advantages:

Advanced Semiconductors: Germanium is used in high-technology applications such as infrared systems, fiber optics, polymer catalysis, electronics, and solar cells. Its superior charge carrier mobility makes it valuable for specialized transistors and next-generation semiconductor technologies. Silicon-germanium alloys enable improved performance in certain integrated circuits, combining the best properties of both materials.

Fiber Optic Communications: Germanium dioxide serves as a dopant in optical fiber cores, enabling precise control of refractive index profiles. This application is crucial for long-distance telecommunications infrastructure that carries internet traffic, phone calls, and data transmissions worldwide.

Infrared Optics: Germanium’s transparency to infrared radiation makes it invaluable for thermal imaging systems, night vision equipment, and infrared spectroscopy. These components are used in night-vision goggles, thermal imaging cameras, and infrared astronomy. Military applications, search-and-rescue operations, and industrial monitoring all depend on germanium-based infrared optics.

Solar Energy: Multi-junction solar cells incorporating germanium achieve exceptional efficiency levels. These cells are standard equipment on satellites and spacecraft, where their superior performance justifies their higher cost compared to terrestrial silicon panels.

Advanced Electronics: Germanium’s high electron mobility makes it excellent for high-speed transistors used in computer processors, communication systems, and radar systems. As the semiconductor industry pushes toward smaller features and higher performance, germanium is experiencing renewed interest as a potential successor or complement to silicon in advanced nodes.

Supply Chain Vulnerabilities

China produces approximately 60% of the world’s refined germanium, though the concentration is less extreme than for gallium. The United States imports about 80% of its germanium from China, creating similar supply chain vulnerabilities.

Global germanium production stands at approximately 130 tonnes annually, primarily recovered from zinc refineries and coal fly ash. The low recovery rates from potential sources mean that germanium’s criticality stems more from lack of economical and efficient extraction processes than from lack of resources.

Mining and processing locations include China, Russia, Canada, and historically Namibia’s Tsumeb Mine. The element’s recovery as a byproduct means that germanium supply depends on economic conditions in the zinc and coal industries, creating additional market uncertainties.

Part Three: Antimony – The Ancient Metal Meets Modern Technology

Ancient Origins and Historical Uses

Unlike gallium and germanium, antimony has been known to humanity for millennia. Fragments of a Chaldean vase made of antimony date to approximately 4000 BCE, making it one of the oldest known metallic materials. Antimony sulfide (stibnite) was used in ancient Egypt as mascara and eye makeup known as kohl, with the famous biblical figure Jezebel being among its notable users.

The Roman scholar Pliny the Elder described several ways of preparing antimony sulfide for medical purposes in his treatise Natural History around 77 AD. Pliny distinguished between “male” and “female” forms of antimony, with the male form being the sulfide and the superior female form likely referring to native metallic antimony.

Throughout medieval and Renaissance periods, antimony occupied a prominent place in alchemy and medicine. The metallurgical text by Vannoccio Biringuccio, entitled De la Pirotechnia (1540), mentioned that metal could be formed from stibnite, predating the more famous work by Georgius Agricola.

The mysterious “Triumphal Chariot of Antimony,” published in 1604 under the pseudonym Basil Valentine, supposedly a 14th-century Benedictine monk but probably written by Johann Tholde, promoted antimony as a cure for syphilis, melancholy, chest pains, fevers, and plague. This influential text detailed various preparation methods and applications, cementing antimony’s place in early modern medicine and chemistry.

Medicinal Applications and Toxic Legacy

Antimony compounds were used medicinally from the 16th century onwards, with Paracelsus largely responsible for their popularity. Tartar emetic (antimony potassium tartrate) became one of the most prescribed medicines in Europe, used as a powerful emetic (inducing vomiting) and purgative.

A particularly successful product called ‘Dr James’ Fever Powders,’ introduced in the mid-18th century, combined antimony with mercury and remained on the market for over one hundred years. The compound was used to treat fevers, infections, and numerous other ailments based on the prevailing medical theory that expelling body fluids could cure disease.

The perceived efficacy of antimony-based remedies persisted despite their dangers, with historical figures including Mozart, King Charles II of England, and Napoleon Bonaparte all believed to have been treated with antimony compounds. Some historians attribute Mozart’s death in 1791 to cumulative effects of antimony-based remedies prescribed for his persistent illnesses.

The popularity of antimonial drugs declined during the 19th century as their toxic effects became better understood, though a reversal occurred at the start of the 20th century after medical applications for treating parasitic diseases were developed. Modern medicine still employs certain antimony compounds for treating tropical parasitic infections, particularly leishmaniasis, though with careful monitoring due to toxicity concerns.

Physical and Chemical Properties

Antimony is a lustrous, silvery-gray metalloid belonging to the nitrogen group on the periodic table, positioned between arsenic and bismuth. It is found in nature mainly as the sulfide mineral stibnite (Sb₂S₃), and occurs in many allotropic forms with different physical arrangements of atoms.

The metallic form of antimony is brittle with a flaky, crystalline texture. It is a poor conductor of heat and electricity compared to true metals, characteristics typical of metalloids. Like water and the elements gallium, germanium, silicon, and bismuth, antimony expands as it freezes, a property valuable in metal casting as it ensures accurate filling of molds.

At room temperature, antimony is relatively stable and unreactive. However, when heated, it burns brilliantly with the formation of white fumes of antimony trioxide. This compound forms the basis for many of antimony’s most important modern applications.

Industrial Revolution and Metallurgical Applications

Antimony became widely used in medieval times, mainly to harden lead for type used in printing presses, though some was also taken medicinally as laxative pills that could supposedly be recovered and reused. The printing revolution depended partly on antimony-lead alloys that provided the hardness necessary for durable, precise type.

Records from the 15th century show antimony’s use in alloys for type, bells, and mirrors. The addition of antimony to other metals improved their casting properties, hardness, and durability, making it valuable across numerous applications from musical instruments to decorative metalwork.

Modern Applications: From Flame Retardants to Defense Systems

Today, antimony’s applications span civilian and military sectors, with growing strategic importance:

Flame Retardants: Antimony trioxide is a prominent additive for halogen-containing flame retardants, representing one of the largest uses of antimony globally. These compounds are incorporated into plastics, textiles, adhesives, rubber, and building materials to slow flame spread and improve fire safety. The synergistic effect of antimony trioxide with halogenated compounds provides cost-effective fire protection for consumer goods, electronics, vehicles, and construction materials.

Lead Alloys and Batteries: The most common applications for metallic antimony are in alloys with lead and tin, which have improved properties for solders, bullets, and plain bearings. In lead-acid batteries, antimony improves the rigidity of lead-alloy plates and enhances charging characteristics. This application remains crucial for automotive starter batteries, backup power systems, and energy storage installations.

Semiconductors and Electronics: Since the 1990s, antimony has been increasingly used in semiconductors as a dopant in n-type silicon wafers for diodes, infrared detectors, and Hall-effect devices. Indium antimonide enables mid-infrared detection capabilities essential for thermal imaging, gas sensing, and spectroscopy applications.

Defense and Ammunition: Antimony is critical to ammunition, communication equipment, night vision goggles, and other military equipment. The element’s importance to defense applications has elevated its strategic significance, with the Pentagon having looked into domestic projects to provide reliable and secure antimony supplies for several years.

Specialized Industrial Applications: Three other applications consume nearly all the rest of the world’s supply: as a stabilizer and catalyst for polyethylene terephthalate production, as a fining agent to remove microscopic bubbles in glass (especially for television screens), and as pigments for ceramics and enamels.

Supply Concentration and Strategic Concerns

China is the largest producer of antimony and its compounds, with most production coming from the Xikuangshan Mine in Hunan Province. China accounts for 48% of global antimony production, with Russia being another major producer.

The United States imports 85% of its antimony supplies, having stopped domestic mining in 2001. This heavy import dependence creates vulnerabilities similar to those for gallium and germanium, particularly given antimony’s importance for military applications.

The historical significance of antimony to US defense was demonstrated during World War II, when antimony and tungsten from the Stibnite Gold mine were credited with shortening the war by one year and saving one million American soldiers’ lives. This historical precedent underscores the strategic importance of secure antimony supplies.

Part Four: Geopolitical Dimensions and Economic Warfare

China’s Dominance and Export Controls

The concentration of gallium, germanium, and antimony production in China represents one of the most significant supply chain vulnerabilities in modern industrial history. China’s methodical capture of the gallium market, rising from zero production in 1980 to 85% global dominance by 2008, represented one of the most successful resource monopolization strategies in modern history.

This dominance stems from several factors: China’s large-scale production of aluminum, zinc, and other metals from which these elements are recovered as byproducts; willingness to tolerate environmental impacts of extraction and processing; government support for strategic mineral industries; and economies of scale that make competition difficult for other nations.

In July 2023, China imposed strict export licensing requirements on gallium and germanium, requiring domestic producers to obtain government approval before shipping these materials internationally. Similar controls were extended to antimony in September 2024. These measures represented an escalation in the ongoing technology competition between China and Western nations, particularly the United States.

In December 2024, China announced an immediate ban on exports of gallium, germanium, and antimony to the United States, coming just one day after the Biden administration imposed expanded restrictions on advanced US technology sales to China. The Chinese Ministry of Commerce stated that “in principle, the export of gallium, germanium, antimony and superhard materials to the United States shall not be permitted”, representing a complete embargo rather than merely tightened licensing.

Price Volatility and Market Disruption

The export restrictions have caused dramatic price movements across all three minerals. Gallium and germanium prices rose by approximately 70% and 190%, respectively, since August 2023 when restrictions were first introduced. Antimony prices reached $39,000-$42,000 per tonne by late 2024, up almost 250% year-to-date, making it the highest performer among all commodities.

Antimony trioxide prices in Rotterdam surged 228% since January 2024, reflecting the severity of supply disruptions. These price increases ripple through supply chains, affecting everything from consumer electronics to military equipment manufacturing.

Chinese customs data revealed no shipments of germanium or gallium to the United States through October 2024, with antimony shipments plunging 97% in October compared to September. This near-complete halt in exports demonstrated the effectiveness of Chinese export controls and the vulnerability of US supply chains.

Industry Impacts and Adaptation Strategies

The semiconductor supply chain has been exceedingly vulnerable over recent years due to ongoing trade tensions, severe weather events, and the COVID-19 pandemic. The addition of critical mineral export restrictions compounds these challenges, forcing companies to adapt rapidly.

US industries must act quickly to diversify supply chains and secure reliable sources of critical materials. Strategies being pursued include:

Diversification of Sources: Companies are establishing relationships with suppliers in Australia, Canada, Bolivia, and other countries with potential production capacity. Australian gallium production expansion, Canadian germanium project development, and Bolivian antimony mining growth represent efforts to reduce dependence on Chinese supplies.

Enhanced Recycling: European recycling capacity building aims to recover these critical minerals from electronic waste and end-of-life products. While recycling alone cannot meet demand, it provides supplementary supply that reduces dependence on primary production.

Technology Substitution: Research into alternative materials that can replace or reduce the need for these critical minerals continues, though finding substitutes with comparable performance characteristics remains challenging.

Strategic Stockpiling: More market sectors are considering strategic stockpiling, expanding beyond traditional niche sectors like medical and defense to include automotive, machinery, and equipment industries. Government-level strategic reserves are also being established or expanded.

Economic Impact Assessments

The US Geological Survey calculated that if China were to halt all exports of gallium and germanium to all countries, the US GDP could face a decline of $3.4 billion. This figure likely underestimates the full economic impact, as it doesn’t account for cascading effects throughout supply chains, technological innovation delays, or national security implications.

The US military’s reliance on advanced technology makes it especially vulnerable to disruptions in critical raw material supplies. Antimony shortages could severely affect military hardware production, flame-retardant materials in defense systems, and next-generation weapons development. Gallium and germanium shortages would impact radar systems, communications equipment, night vision devices, and countless other defense technologies.

The semiconductor industry faces particular challenges. With the lion’s share of global production of gallium, germanium, and antimony, China’s export ban has triggered significant supply chain issues. Companies cannot simply switch suppliers overnight, as establishing new production facilities requires years of investment and development.

Part Five: Future Outlook and Strategic Responses

Temporary Relief and Ongoing Tensions

In 2025, China suspended export restrictions on gallium, germanium, and antimony to the United States until November 27, 2026, following high-level diplomatic meetings. This suspension provides immediate relief while highlighting the ongoing need for supply chain resilience planning.

However, the temporary nature of the suspension emphasizes continuing risks, as future restrictions could be reimposed based on geopolitical developments. The suspension maintains the underlying export control framework, requiring Chinese exporters to obtain licensing for overseas sales, demonstrating that the strategic leverage remains in place.

Long-term Market Outlook

The long-term outlook for these metals remains uncertain, with two primary scenarios: prices falling as geopolitical tensions cool, or continued elevated prices if tensions persist. The base case scenario assumes eventual price declines as tensions ease and alternative supplies develop.

Despite bullish medium-term forecasts, prices would likely fall the moment export restrictions are permanently lifted, as China’s production dominance could quickly flood markets. This creates significant risks for companies and countries investing in alternative production capacity, as their higher-cost operations might become uneconomical if Chinese exports resume at full scale.

There is excess production capacity for gallium and germanium in China, with tightness in antimony markets due to political instability in key producing regions. This overcapacity means China could rapidly increase exports if it chose to do so, potentially undercutting alternative suppliers.

Domestic Production Initiatives

The United States and allied nations are pursuing various strategies to reduce dependence on Chinese critical mineral supplies:

Mining and Processing Development: New projects aim to extract and process these minerals domestically or in friendly nations. However, the economics remain challenging, as these elements are primarily recovered as byproducts rather than mined directly.

Technology Innovation: Research into more efficient extraction and recovery processes could make previously uneconomical sources viable. Improved, efficient, and economical production methods utilizing unconventional resources could reduce supply risks.

Policy Support: Government initiatives including the CHIPS Act in the United States provide funding and incentives for domestic semiconductor manufacturing and critical mineral supply chain development. Similar programs in Europe, Japan, Australia, and other countries aim to build more resilient supply chains.

International Cooperation: Partnerships between allied nations can distribute production capabilities and reduce individual country vulnerabilities. The development of processing facilities in multiple countries creates redundancy and resilience.

Technological Applications Driving Demand

Demand for all three minerals continues growing, driven by expanding applications:

Artificial Intelligence and Data Centers: AI data centers are projected to drive 2% of global copper demand by 2030, with similar increases expected for gallium and germanium in advanced semiconductors powering AI systems.

5G and Beyond: Next-generation telecommunications infrastructure relies heavily on gallium nitride power amplifiers and other gallium-based components. The global buildout of 5G networks and future 6G development will sustain strong demand.

Renewable Energy: Solar panels, particularly high-efficiency cells for space applications and concentrated solar power, increasingly incorporate gallium and germanium. The global transition to renewable energy supports long-term demand growth.

Electric Vehicles: Advanced power electronics in electric vehicles use gallium nitride semiconductors for more efficient power conversion. As EV adoption accelerates, this application will become increasingly significant.

Defense Modernization: Military forces worldwide are upgrading electronic systems, with programs requiring advanced semiconductors, infrared systems, and communications equipment that depend on these critical minerals.

Conclusion: The Strategic Imperative

Gallium, germanium, and antimony represent far more than technical curiosities on the periodic table. These three elements have become critical enablers of modern civilization, essential to technologies that define contemporary life and national security. Their unique properties—gallium’s exceptional electronic characteristics, germanium’s optical and semiconductor capabilities, and antimony’s fire-retardant and alloying properties—cannot be easily replicated by substitutes.

The concentration of production in a single nation creates unprecedented vulnerabilities in global supply chains. These raw materials are indispensable for modern semiconductor production, and without them, Western technology companies cannot manufacture their chips and electronic components. This reality has transformed these

Be First to Comment